Executive Summary:

- International developed markets experienced significant volatility, with the MSCI EAFE Index delivering a strong 10.1% return in the first two months of 2026 but reversing to a -10.2% return in March following geopolitical tensions in Iran.

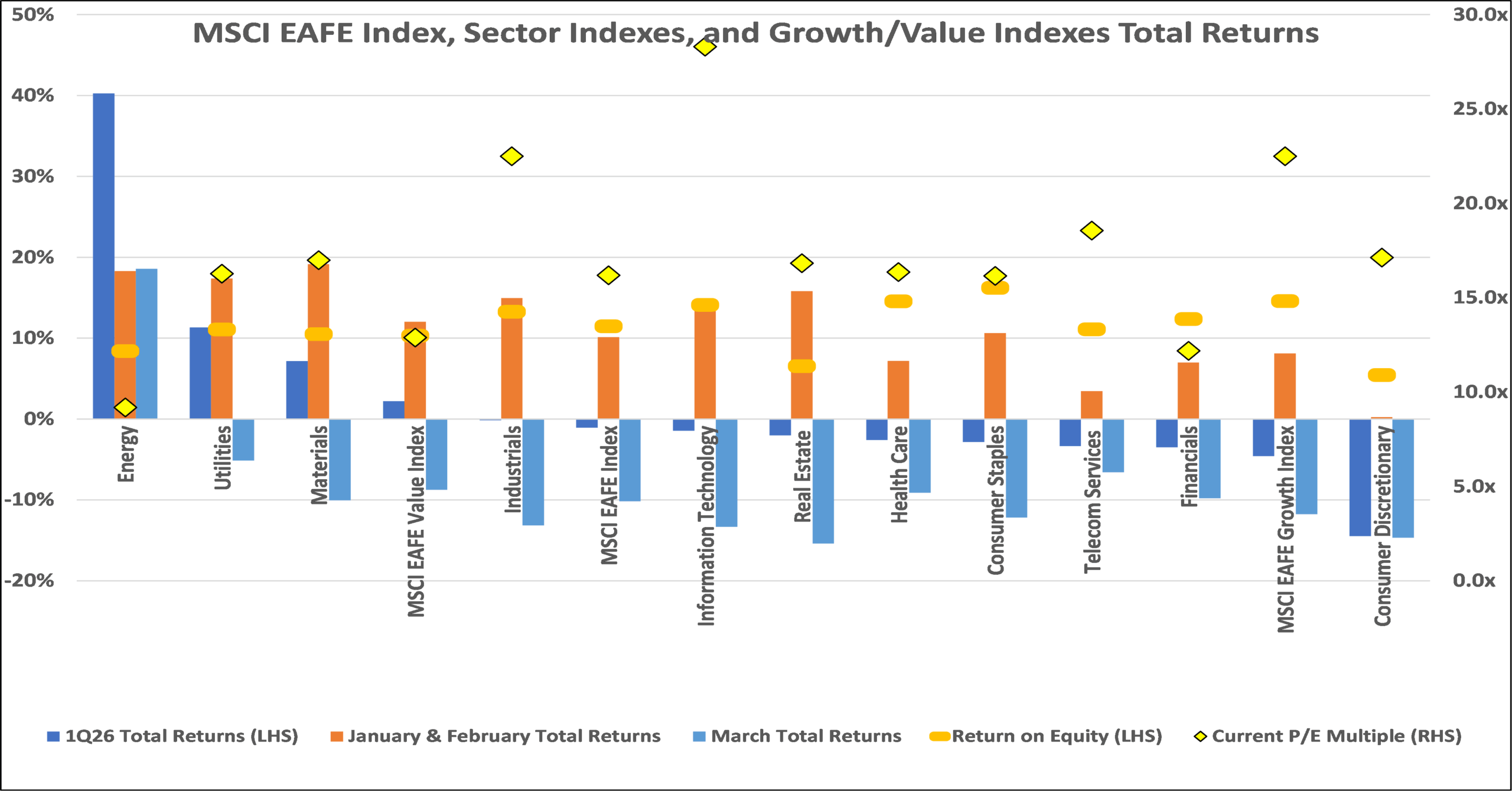

- For the whole first quarter, the index was down 1.1%, with Energy, Utilities, and Materials as the only sectors in positive territory.

- High-quality stocks continued to underperform the broader index, with the MSCI EAFE Quality Price Index returning -3.5% during the quarter.

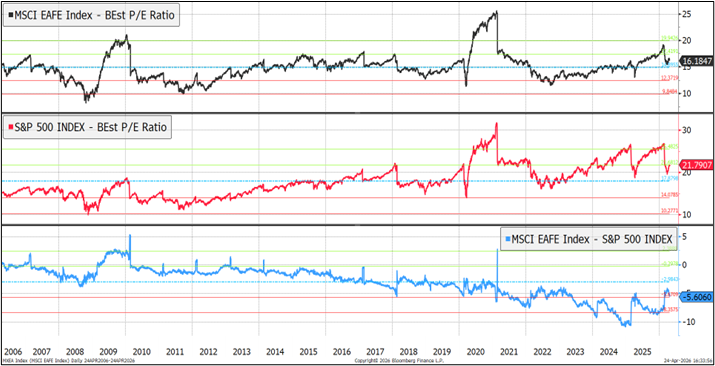

- Valuation gap between U.S. and international equities remains notable, as international companies continue to trade at a discount to their U.S. counterparts – much of this difference results from sector composition and growth prospects.

- Entering 2026, international markets face a complex environment:

- Europe is experiencing easier financing conditions but remains constrained by fiscal challenges. Negative balance of trade for energy has tempered growth outlook.

- China’s economy is increasingly reliant on exports as domestic investment and consumption remain soft, heightening the risk of trade tensions

- Japan continues to grapple with sluggish growth and demographic headwinds, though maintaining accommodative monetary policy despite above-target inflation.

- Canada’s outlook remains subdued, with stagnant productivity and a likely pause in monetary policy.

Economic and Capital Markets Commentary

International developed markets, like domestic markets, were a tale of two regimes, with the MSCI EAFE Index reversing course after a strong start to the year. The total return for the index was 10.1% during the first two months of the year with broad-based sector performance. After the commencement of kinetic action in Iran, the index returned -10.2% in March, with only one sector positive for this period (Energy). For the full first quarter, the MSCI EAFE Index returned -1.1% with only three sectors, Energy, Utilities, and Materials, providing positive returns.

Within the EAFE family of indexes, value stocks remained clear winners as economic stress, price inflation, and interest rate trajectory came under greater scrutiny through a renewed stagflationary lens. MSCI EAFE Value outperformed with a total return of 2.2%, exceeding the MSCI EAFE Growth Index’s -4.6% return by 680bps. The quality factor continued to underperform the broader index, as the MSCI EAFE Quality Price Index returned -3.5%. This trading dynamic is eerily similar to 2022, when inflation pushed restrictive monetary policy into decelerating economic growth. Style indexes have – at this point – responded similarly to the stressors.

The chart below shows the sector-performance, and Energy was the only sector that performed well in both regimes. Consumer Discretionary was the greatest laggard, as the velocity to escape the K-shaped consumption pattern appears elusive, with new risk developing from an oil “tax” on households. Other rate-sensitive sectors also lagged, with Real Estate (financial leverage) and Information Technology (discount rate) leaders to the downside in March.

Source: Bloomberg LP

Source: Bloomberg LP

While valuation multiples for international companies in the index compressed, the chart below displays that they remain at steep discounts to their U.S. peers. I would note that the index constituents and sector weights influenced the willingness to accept lower implied discount rates. The faster rate of earnings growth, driven by greater exposure to technology, and sustainably higher return on equity have maintained the premium multiple for U.S. companies, despite current risks of higher discount rates.

North America

In early 2026, the U.S. economy has remained resilient despite a challenging mix of higher interest rates and global energy shock, related to operations in Iran. Growth continued at a solid pace, supported by business investment – particularly, in technology – and AI-related capital spending, while the labor market has cooled but not cracked, with job gains slowing and unemployment roughly steady. Inflation, however, proved sticky and may be vulnerable to energy price swings, as higher gasoline and transportation costs filter through to overall household spending and selected goods categories.

Looking ahead to the rest of 2026, the base case is for moderating, but still above-target, inflation and a slowdown in activity as tighter financial conditions and higher energy costs weigh on real incomes, housing, and rate-sensitive demand. At the same time, ongoing technology capex and improving productivity trends should help keep the economic expansion intact, making recession a risk rather than a central scenario. The key swing factors are how quickly energy markets normalize, whether inflation pressures broaden beyond energy and shelter, and how the Federal Reserve responds – potentially, staying on hold longer or delivering limited easing.

Canada’s economy is showing modest growth in early 2026, despite facing significant headwinds from trade uncertainty and after a challenging 2025. First quarter real GDP growth is estimated at 1.5% annual rate, a meaningful acceleration from the -0.6% recorded for fourth quarter growth (annualized). The economy posted a 0.1% month-over-month gain in January, followed by a stronger 0.2% advance in February, exceeding initial expectations. Inflation in the quarter averaged 2.2% annualized rate, remaining close to the Bank of Canada’s target, while unemployment stood at 6.6%, retreating from a high of 7.0% last September. However, the outlook for the remainder of 2026 has been revised downward, with economists now forecasting full-year GDP growth of just 1.1%, as the Middle East conflict drives up energy prices and inflation expectations. While the economy may still hit a soft patch in the first half of 2026, several forces should support a recovery later in the year and into 2027, including fading tensions and improving domestic demand. The Bank of Canada is expected to maintain its benchmark rate at 2.25% through year-end as policymakers balance growth concerns against inflation pressures.

Western Europe

Early-2026 European data were cooling even before the latest geopolitical flare-up, as exhibited in the Composite Purchasing Managers’ Index (PMIs) slide towards contraction, driven by weakening services. Alternatively, European manufacturing activity actually accelerated during the first quarter. The euro area manufacturing PMI rose from 49.5 in January to 51.6 in March, crossing above the 50 threshold that separates expansion from contraction and reaching the strongest level of the quarter. Unfortunately, consumer confidence indicators fell to levels not seen since 2022 in March, coinciding with the Russian invasion of Ukraine and related disruption of energy supplies. Current surveys of households’ expectations for further deteriorating economic conditions over the next twelve months could temper support from domestic consumption.

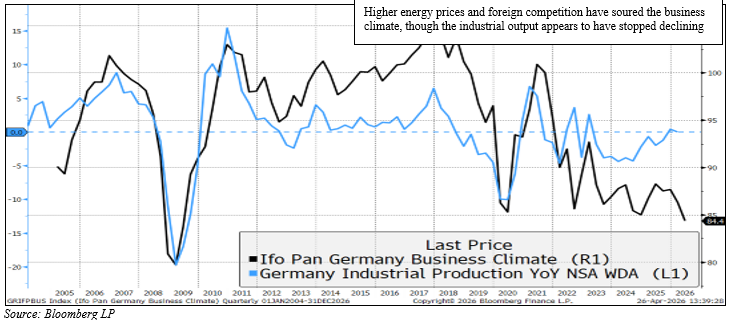

Germany’s economic outlook has sharply deteriorated as the Iran war drives up energy costs and undermines business confidence, threatening to derail what had been a nascent recovery in Europe’s largest economy. Though the Manufacturing Purchasing Managers’ Index (PMIs) were firmer than early estimates, this resilience may fade if the conflict persists. Economists have recently marked down Germany’s expected annual-average real GDP growth to about 0.7% (from 1.3% previously), and this revised annual growth will be supported by a potential reacceleration during the second half of the year. Business sentiment has collapsed, with the Ifo Business-Climate Index plunging to 84.4 in April from 86.3 in March, marking the lowest level since May 2020 during the COVID-19 pandemic. German private-sector activity unexpectedly contracted in April, with the Composite PMI falling to 48.3 from 51.9 in March, dropping below the 50-threshold for the first time since May 2025. The conflict with Iran triggered the biggest plunge in the services sector in more than three years.

Manufacturing has shown resilience, with the PMI rising from 49.1 in January to 52.2 in March before edging down to 51.2 in April, ending a prolonged slump that had curbed economic and jobs growth since 2022. However, this strengthening in manufacturing has been insufficient to offset the sharp deterioration in services, which fell to 46.9 in April from 50.9 in March. Headline inflation accelerated from 1.9% in February to 2.7% in March, and real retail sales growth slowed from 1.6% in January to 0.9% in February. Fortunately, unemployment has held steady at 4.0%. The Bundesbank noted that the economy probably grew “modestly” in Q1 but sees “another modest expansion at best” in Q2, while the central bank expects inflation to remain “significantly elevated”. With fiscal policy expected to offer increasingly positive impulses from vast government outlays, Germany faces a balancing act between supporting growth and managing inflation in an environment of elevated energy costs and weakening consumer confidence.

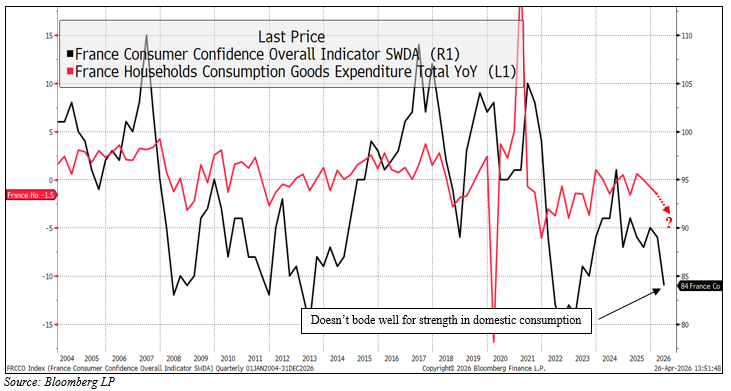

France’s economic outlook has deteriorated markedly in recent weeks, with mounting evidence of pressures as the Iran war weighs on consumer confidence and business activity. French business activity shrank at the fastest pace in more than a year in April, with the Composite PMI dropping to 47.6 from 48.8 in March, marking a fourth consecutive month below the 50 threshold and reaching a 14-month low. The decline was driven by a steep contraction in services, where the PMI fell to 46.5, as the Iran conflict made consumers more cautious about spending. Consumer confidence plunged to 84 in April from 89 in March, the largest monthly decline since March 2022, with households growing increasingly pessimistic about their personal financial situation, unemployment prospects, and price evolution. Inflation accelerated sharply, rising from 0.3% annualized rate in January to 1.7% in March, and the government has trimmed its growth forecasts for the next three years. Economists have revised GDP growth to just 0.9% for 2026, down from prior forecasts of 1.0%, with quarterly growth projected to slow to just 0.1% in Q2. The one bright spot has been Manufacturing PMI, which expanded to a 47-month high of 52.8 in April. This strength has been insufficient to offset the broader weakness in the dominant services sector. With unemployment rising to 7.9%, retail sales showing minimal growth of just 0.1% year-over-year in March, and industrial production contracting 0.3% in February, France faces a challenging path ahead as it attempts to narrow its fiscal deficit to below 3% of GDP by 2029 while navigating external shocks and weak domestic demand.

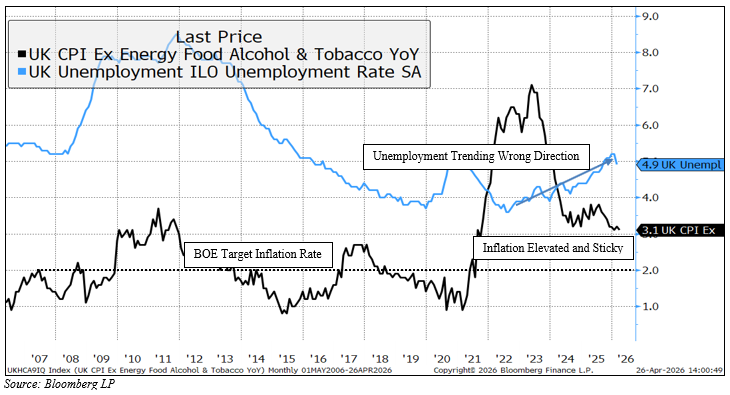

Looking through the rest of 2026, Europe’s economic trajectory hinges on (1) the duration and severity of the energy shock, (2) how quickly financial conditions stabilize, and (3) central-bank reaction functions. The Bank of England will be most challenged with balancing financial accommodation with a weakening labor market without compounding price volatility. On the flipside, a de-escalation that lowers energy costs would improve confidence and reduce the need for restrictive policy. Continued disruption (or policy missteps that raise yields/credit spreads) would likely stall growth, with the U.K. most exposed, Germany constrained by its industrial structure, and France likely tracking a broader euro-area slowdown.

The U.K. stands as a particularly vulnerable major economy. It entered the Iranian conflict with weak labor-market fundamentals, a large negative terms-of-trade around energy, and among the tightest financial conditions. Prior to the conflict, the U.K. was flirting with recession, with unemployment rising toward the mid–high 5% range from a low of 3.6% set in 2022. A move higher in unemployment is likely, alongside an elevated risk of the U.K.’s technical recession. Over the last two quarters, the quarterly real GDP growth rate has remained weak, decelerating to only 0.1% quarterly rate during the fourth quarter. This puts the Bank of England in a difficult position. Headline inflation may re-accelerate into the high 3-4% area as energy passes through, and yet, labor slack and weaker demand argue against higher policy rates. With a single mandate for price stability, the central bank could be more inclined to respond to inflationary risks, despite a weakening labor market. A weaker consumer could temper some demand-driven influence on inflation in a supply-constrained environment, but the disruption reintroduces the risks of stagflation.

Asia Pacific

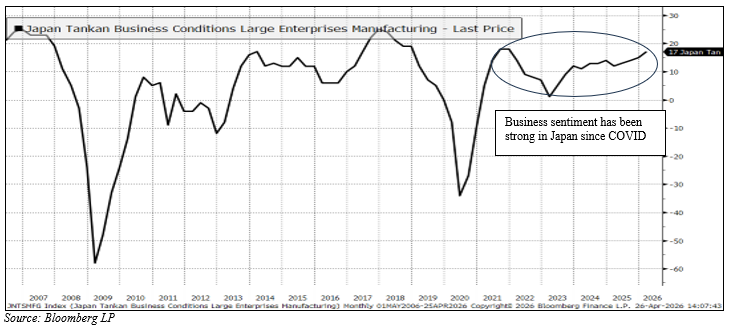

Japan’s economic outlook is stronger than that of its European counterparts, with manufacturing activity surging to multi-year highs even as inflation pressures build and service sector growth moderates. In Q1 2026, Japan’s economy expanded 0.6% year-over-year, while headline CPI inflation was 1.6%. Business sentiment stayed firm, with the Bank of Japan’s Tankan for large manufacturers improving for a fourth straight quarter to 17, its highest level since late 2021, though forward-looking components began to soften. Activity indicators for Japanese manufacturers exhibit ramped-up production in April, with the S&P Global Manufacturing PMI climbing to 54.9, the strongest reading since January 2022, as the factory output index reached 55.4, the highest since February 2014. External accounts surprised to the upside as Japan posted a ¥57.3bn trade surplus in February, supported by technology exports and shipments to Europe. Despite some stronger data, Japan remains exposed as a net energy importer with the yen near historic lows. Offsetting manufacturing and export strength, service sector expansion slowed, with the services PMI dropping to 51.2 in March, pulling the composite PMI down to 52.4 from 53.0, marking the weakest pace in four months though still indicating expansion for the 13th consecutive month.

Looking ahead, most forecasters expect slower but still positive growth in 2026 for Japan, with median estimates around 0.7% real GDP growth, as domestic demand and capital spending provide support. Consumption should stabilize as wages rise and inflation eases, but we could expect some near-term momentum to fade as one-off tailwinds, such as front-loaded exports and inventory rebuilding, diminish for this export-driven economy. Manufacturing may see softer growth into late 2026, and higher energy costs remain a key downside risk to household spending.

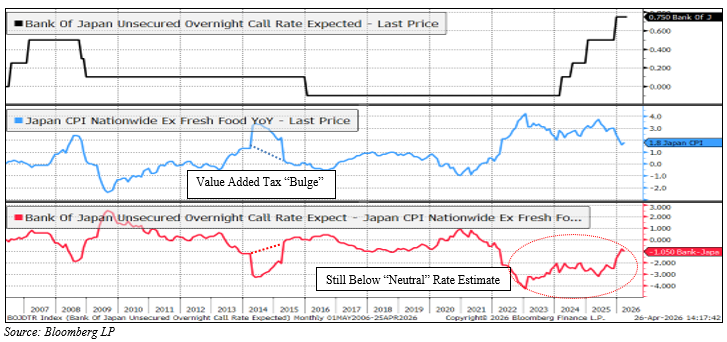

On policy, expectations generally point to gradual normalization, with pundits anticipating two Bank of Japan rate hikes over the next year. Japan’s core inflation accelerated to 1.8% year-over-year in March, topping economist estimates of 1.7% and marking the first acceleration in five months. The inflation reading, which excludes fresh food, remains below the Bank of Japan’s 2% target for the second consecutive month. The main question for the outlook is whether improving wages, low unemployment, and capital investment can offset energy-price, external-demand, and confidence shocks, as the Bank of Japan must remain vigilant in its price stability mandate.

Despite relative strength, risks remain skewed to the downside for Japan, including prolonged war-related headwinds, renewed Sino-Japanese tensions that could weigh on tourism and trade, and structural demographic pressures. Fiscal sustainability is also a concern, with deficits expected to widen even as ratings agencies continue to cite Japan’s strong external position and diversified economy as offsets to its debt burden. A prolonged energy shock would likely hit real incomes and consumption, slowing progress toward durable, demand-driven domestic expansion. Even so, the baseline remains for steady expansion supported by domestic demand, with policy rates continuing to rise only gradually. Further fiscal or targeted stimulus could partly cushion downside scenarios but may add to longer-run debt tradeoffs.

Australia’s economy is navigating a challenging environment in 2026 as the Middle East conflict drives a sharp acceleration in inflation and forces the Reserve Bank of Australia into a tightening cycle. The Australian economy may head into a sharp slowdown in 2026 as the energy supply shock and persistent inflation led the RBA to raise interest rates. Economists have lowered their real GDP growth forecast to 2.0% for 2026, while raising the annual inflation outlook to 4.1%. The IMF has warned that Australia is projected to have one of the highest inflation rates among developed countries. Inflation expectations surged in April to the highest level since November 2022, driven largely by a spike in oil prices. The unemployment rate stood at a manageable 4.2% during the first quarter, actually receding slightly from the high of 4.3% set late last year. Consumer confidence fell to its fourth-lowest level on record since 1973 as higher fuel prices and soft sentiment weighed on spending. Unfortunately, the Reserve Bank of Australia is expected to raise its cash rate target to 4.35% in the second quarter from the current 4.10%, as the supply shock knocks the RBA off its “narrow path”.

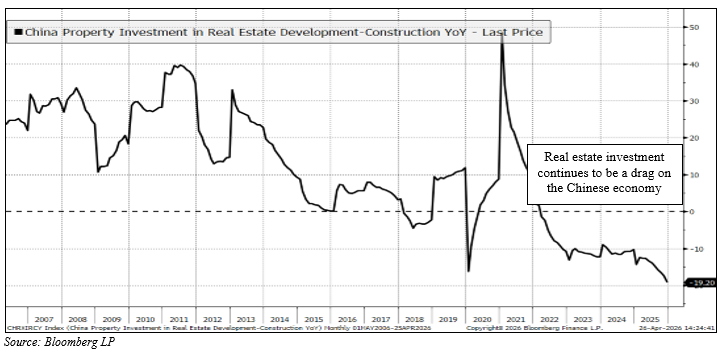

China’s economy started 2026 with headline strength but an increasingly unbalanced mix. Real GDP rose 5.0% y/y in 1Q, according to “official” sources, an acceleration from 4.5% in 4Q25, helped by firm industrial activity and – most importantly – strong net exports. That external lift masked ongoing softness on the home market, where retail sales’ growth slowed to a 1.7% annual rate in March, fixed-asset investment rose at only a 1.7% annual rate in the first quarter, and the property downturn persisted with real estate investment declining 11.2% through March. Price dynamics continued to reflect this imbalance, though upstream pressures improved with PPI turning positive in March, rising 0.5% from the prior year.

The key story in the first quarter was that exports did the heavy lifting to promote aggregate growth, but momentum already showed signs of cooling late in the quarter. China’s exports surged during the first two months and then slowed sharply to rising at 2.5% annual rate in March, as the Iran-war-driven energy shock and broader uncertainty began to weigh on global demand and supply chains. This deceleration reinforces the broader concern that China’s growth model has become more dependent on foreign demand at a time when trade frictions, anti-dumping scrutiny, and geopolitical spillovers are rising, making an export-led quarter a less reliable template for the rest of the year.

For the full year, the economic forecasts remain consistent with Beijing’s 4.5%–5% target range, but there remains a downside skew until domestic demand stabilizes. The most plausible path is moderation from recent pace as (1) the export impulse fades, (2) higher energy costs compress margins (3) elevated energy costs limit real purchasing power abroad, and (4) property markets and consumer confidence remain drags on household spending. Policy is likely to lean on incremental fiscal support for infrastructure and “new quality productive forces” rather than broad-based support for domestic consumption. China can likely make the number, but growth looks more fragile because it continues to be carried by the least controllable component, external demand, rather than a durable domestic recovery in consumption.

In summary, the outlook for global growth in 2026 remains highly uncertain and challenged by an escalating array of geopolitical risks. The continuing US-Iran conflict and broader Middle East instability have not only driven energy prices sharply higher—Brent crude well above $100 per barrel—but also raised the specter of stagflation and recession in major economies, amplifying supply-side shocks. Strategic shipping lanes, critical energy infrastructure, and global oil and gas flows are at risk from prolonged conflict, while tariff escalation and ongoing US-China strategic tensions add further headwinds for trade and investment. The war in Ukraine, instability in the Middle East, and the potential for flashpoints such as US-China friction over Taiwan continue to cast a shadow over global economic prospects. These developments, combined with the fracturing of the US-centered, rules-based order and persistent uncertainty across energy markets, commodity prices, and trade routes, reinforce the downside risks to growth. As outlined in our geopolitical risk framework, policymakers and investors must remain vigilant to these multifaceted risks, which have the potential to deepen financial volatility, disrupt international commerce, and reshape the global economic landscape over the years ahead.

Mason D. King, CFA

May 7, 2026